Namaskar, my name is Rupesh Jadhav, and welcome to Rupeshfinancialexpert.

Where I unlock financial knowledge. In this Blog, I’m going to talk about Credit cards. Nowadays everyone has a credit card and having 1-2 credit cards is very common. But some people also have 6-7-8 credit cards. Since nowadays online shopping is very common, some websites give discounts on any credit cards, another website offer discount on another credit card. Many people think that they can increase their credit card period, by keeping multiple credit cards. Payment of 1st done through 2nd and of 2nd through 3rd. But are there any advantages of having a credit card? Or it has more demerits? I’ll be discussing this in this Blog. In fact, I also made a Blogs on ‘Hidden charges of credit card’. So, you can read it. In this blog, I’ll talk about the advantages and disadvantages of credit card. And in the end, I’ll give you some tips on how to use credit cards smartly. so, read this blog start to end.

First, let’s try to understand what actually a credit card is and why should we use it? What is Credit Card & Why should you take it? And we will talk about both pros and cons. Firstly, if we talk about credit cards, it is plastic money, it is similar to the currency notes with which we can buy anything by giving that note. Or if you eat food in any restaurant, book a traveling ticket, wherever note is accepted, credit cards are also accepted. So, you can do the payments at outlets, do shopping, can pay a restaurant bill, pay for petrol at petrol pumps, you can do online payments on E-commerce platforms, Or any other type of online financial transactions And third, you can also withdraw cash from the ATM. So these are the main 3 functions.

I’ll talk about should withdraw ATM cash or not in detail, but you can do all these 3 things with credit cards which you can do with currency notes. Now a question arises that how can get a credit card? It basically depends on your salary and also on your CIBIL score. CIBIL score talks about the credit history in past. That means your CIBIL score depends upon, whether you did timely payments of the loan or not. What is the CIBIL score, how you can check it, how to improve it? I made separate blogs on these so you can read them.

Now let’s talk about the advantages and disadvantages of credit cards. Advantages of Credit Card. let’s first discuss the advantages. It is a safer way to carry cash. That means you don’t need to carry cash, suppose you get Rs. 1 lakh limit on your credit card, so it’s not easy and safe to carry Rs. 1 lakh in the form of cash, but you can easily carry a credit card with Rs. 1 lakh limit. And if you want to increase the limit and your salary allows, so you can increase your limit further., Second, you get the record of all the things you bought, so if you had any conflict with the merchant or any third party, you could show the record. Now, what are the disadvantages?

Disadvantages of Credit Card, the biggest disadvantage is that if you delay the payment, High interest rates are charged, and many other charges are also added. If we talk about the interest rates, they charge around 36-40% per annum, which is the highest among any loan or credit. A personal loan is also available at 18-24% but here the interest rates are very high. Also, there are many charges added like finance charges, late payment fee. In fact, I already made a blog on the hidden charges of credit cards so you can read that. 2nd big disadvantage is, if you default payment, your CIBIL score also decreases, and bad CIBIL score means you will not get a loan or credit card easily in the future. And once the CIBIL score decreases, it takes time to improve it. These were the advantages and disadvantages.

Now I am telling you 2-2 advantages and disadvantages. Now question arises that is credit card beneficial or not and should we use it? It depends on how you use it. If you use it smartly then definitely you should have one. And since most people use it smartly, it becomes convenient for them. But let’s see how to use it smartly. What is an Interest-Free Credit Period? But you might have heard about the Interest-Free, Credit Period whenever you get a call from credit card sellers. They say that no interest will be charged on things for 50 days. What does it mean? If, you get interest free period of 20-50 days, what does it mean?

Suppose I am taking an example, assume your bill was generated on 5th July and the due date for payment is 25 July. So, you clearly got a free credit period of 20 days. And let’s say you did shopping on 6th May. So, from 6th May to 5th July, you got 1 month. And if you will add this, you get a free credit period of 50 days. So basically, if you shop on the next day of bill generation, you get a free credit period of 50 days, and if you shop in between, suppose if you did shopping on 15th May, Then you’ve got 20 days from 15th May to 5th July, and 20 days here so you’ve got a free credit period of 40 days. So free credit period depends on your shopping date, Minimum it is of 20 days and maximum it is of 50 days. But the most important thing is, If you default payment, let’s say 25th July, is the due date and you didn’t cleared the due amount, Then interest will be charged from the date of purchase which is 6th May. So, you have to pay interest for the complete 50 days. You’re getting a free period only if you’re clearing the dues on time otherwise you will have to pay full interest. So, keep this in mind.

Should New People take credit Cards? Now let’s discuss should new people use credit cards. People having a bad experience with credit cards, tell their family members and friends to stay away from a credit card, because they had losses. But this is not right. You should definitely use a credit card, because if you use it smartly, it becomes very convenient for you, and how can you use it smartly? Use it according to your payment capacity, you get too much credit limit but don’t use it according to that. I am telling you a rough rule, do not spend more than 50% of your monthly salary. So basically, if you spend according to your payment capacity, you will not spend much and you won’t adopt credit-hungry behaviour. And always pay your full due amount, because your CIBIL score can decrease on doing the half payment. So also keep the CIBIL score in mind.

Many times, we see ‘Minimum Amount Due’ in the credit card statement which is a trap. It means they are asking you to pay interest payment or minimum charges. And you have to pay the interest on the due balance, I am explaining to you with an example. Let’s say your total due is Rs. 1 lakh and 25th July is the due date. And you’re said to pay Rs. 6000 as the minimum due, now if you pay only Rs. 6000, you’ll be charged interest on the remaining Rs. 94,000 25th July onwards. In fact, not from 25th July, From the date of shopping. suppose you shopped on 6th May, then interest will start from 6th May at the rate of 36% per annum. That’s why you should not pay the minimum amount due and only pay full amount. Otherwise, your CIBIL score will also be affected, and interest will also be charged high. so these were the precautions.

Now let’s discuss what to do if you’re already trapped in credit card debt. How do I get out of Credit card Debt? Firstly, you can delay the non-essential items which you don’t need in day-to-day life. So please delay them and clear credit card payment first. if you get a bulk payment. Secondly, you should pay with credit card dues before any other loan. because, as i told you before, its interest rate is 36-40% which is the maximum. so, clear it first and delay other loan repayments. No problem with that. In fact, you can borrow another loan for credit card payment. If you already have a home loan, then on that you can borrow a top-up loan. Because the interest rate for home loans is very less. You can also borrow a personal loan to pay with credit card dues.

There are 2-3 advantages of taking another loan 1. You get better interest rates. If you take a top-up loan then you may get it at 10% per annum interest rate, if you take a personal loan, you get an easy 18-20% interest rate. 2nd. You can pay principal and interest together. suppose you are trapped in a debt trap, so now you would think to keep paying the minimum amount. and you don’t have much capacity to pay more. In this case, the principal amount is not decreasing, but if you borrow a loan, the tenure becomes longer. I am explaining this with an example. assume take that previous example, suppose say you have a total of Rs. 1 lakh credit card due, now if you convert it into EMI and borrow a personal loan, and instead of 1 lakh, you start paying Rs. 10000 per month. Now in this 1 lakh, maybe Rs. 10,000 is the minimum due, and it may be late payment charges and interest charges. And your principal will never reduce, but if you convert it into a personal loan and repay Rs. 10,000 per month, and your interest rate is 18%, so both your principal and interest will start decreasing. But in this case, 1 lakh amount is as it is, and interest rates are also very high. So, you have both the benefits. Interest rate is also charged less, and monthly payment also decreases.

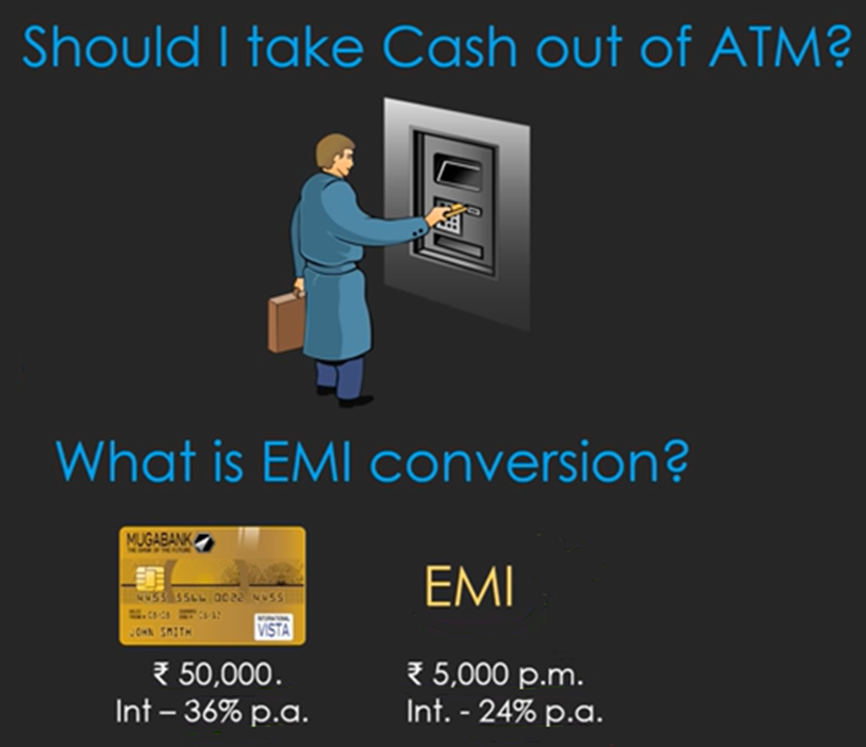

Now the next question is whether you should withdraw cash from ATM or not? Should you take cash out of ATM? So, you should not withdraw cash until you have an extreme emergency situation. So only withdraw cash if you have an extreme emergency. Because if you will withdraw cash using a credit card, they will start charging 36-40% of interest immediately. Interest will start from the day of withdrawal that means you don’t even get interest free period. That’s why I won’t suggest you withdraw cash from ATM using a credit card. If it’s not urgent, don’t do it.

Now there’s one more thing we hear about What is EMI Conversion? Credit card sellers or banks ask us to convert the due amount into EMI, what does that mean? So basically, credit card debt is converted into an EMI option. For example, let’s say Rs. 50,000 is your due amount on a credit card. And you have to pay it immediately within 1 month with 36% interest on that as well, if you don’t have Rs. 50,000, then you will be charged an interest rate. So, in this case, if you convert it into EMI, suppose say you have to pay Rs. 5000 per month. And bank charges less interest rate which is 24%. But is this EMI option best for you? It’s not necessary, you have to calculate it. So definitely you’re getting less interest and tenure increased. Maybe you can pay EMI’s in 12 months. But here you have to pay Rs.50,000 in one month, So, you can choose the EMI option for 12 months and pay Rs. 5000 per month. But calculate effective interest first because sometimes it is too high. Sometimes banks give 1.2 % per month effective or reducing interest. But when you will calculate its IRR by making a schedule on an excel sheet, then you’ll see that the interest rate is 24-30%. So do your calculations before. In fact, if you borrow a personal loan, it comes out as a better option. because you are sure that if you’re getting an 18 % interest rate, then you have to pay 18%. But definitely, if you find the EMI option better then you can definitely go with that.

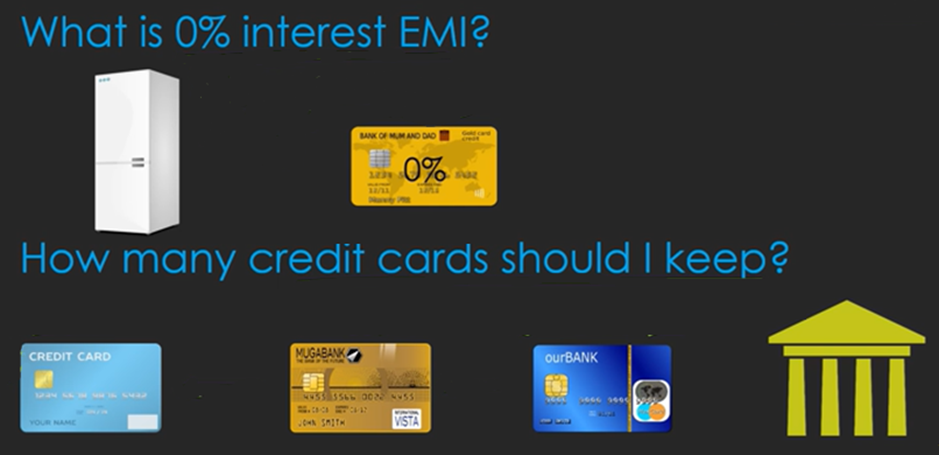

If I talk about 0% interest EMI. What is 0% Interest EMI? We usually hear that we have 0% interest EMI on our credit card, what does it mean? We get 0% EMI but, in that case, whatever you are buying, maybe you’re buying it on MRP or at a much lesser discount. So, in this case, the credit card company directly takes money from the seller company. For example, if you buy a fridge worth Rs. 30,000 which is its MRP. If you go in the market to purchase it, suppose you get a discount of Rs. 3000 easily. So effectively it costs you Rs. 27000. But if you buy it on 0% EMI through a credit card, Chances are that it will cost you Rs. 30,000 and Rs. 3000 which was the discount, goes to the credit card company. In this way, the credit card company earns in this case. So, 0% interest should not be the main motivation for you to take a credit card. And you can calculate that if you’re getting a discount along with the 0% interest then there’s no problem you can use it.

Lastly, a question arises that how many credit cards should I use? How many credit cards should I keep? So, as I told you in the beginning that many people keep 6-8 credit cards also. So, is that right and recommended? According to me, it’s not recommended, and 1-2 credit cards are sufficient. Generally, all the discounts are available on all the cards at different times, or you can also use credit cards of your family members, if you want an online discount. And if you’re taking a credit card for an online discount then you have to manage it also. There are many things to keep in mind to manage your credit card, you may be charged Annual charges or if that is waived. then you’re said to do a minimum number of transactions in a year. The chances of defaulting also increase and if that happens, your CIBIL score gets affected and you’ve to pay high-interest rates. So, it’s better to keep 1-2 credit cards that is easily manageable. Otherwise, how many credit cards you will buy? Because discounts keep coming on different credit cards. And one more thing I would like to answer is that, People say that I’ll do the payment of 1st card through 2nd one and of 2nd through 3rd one And like this, the credit period will keep on increasing.

So, I am taking an example. suppose you have 3 credit cards, and you have to pay Rs. 50,000 on this credit card, you pay that amount through 2nd credit card and now the liability is shifted to this one. Now you did the payment of the 2nd card with the 3rd one and now liability shifts to the 3rd one. Now liability for 1st credit card is free now and you can again pay, you can absolutely do that, but the liability comes again on it. But where this liability is ending? It’s not ending, just your credit period is increasing. But by chance, if you have to buy something worth Rs. 15,000, You’re not paying this liability of Rs. 50,000, because you don’t have money. So how will you buy the other things if it’s your requirement, that’s why I always say, spend according to your payment capacity. Because at some time, you have to end this liability. Until you won’t pay the remaining Rs. 50,000, It will not come to 0.

So, I think I covered all the major points related to credit cards. So, I hope you will be able to use your credit cards smartly after reading this blog. So that’s it in this blog post, if you want to share something related to this website or blog, then do write it in the comment section. In fact, you can suggest the topics for future blogs. And if you liked this blog, Then the like and share it I share these informative finance blogs daily on this website. So, we’ll meet in the next blog.

Till then keep learning, keep earning, and as always, stay happy.